Blockchain Technology

Introduction:

Intro 1:

Blockchain technology is a decentralized and distributed digital ledger that records transactions across multiple computers in such a way that the recorded transactions cannot be altered retroactively. This ensures the integrity and security of the data.

Intro 2:

Blockchain technology is a sophisticated method for securely recording information in a way that makes it difficult or impossible to change, hack, or cheat the system.

Intro 3:

Blockchains are secure digital ledgers where information is bundled into blocks and cryptographically chained together. This makes tampering nearly impossible, as changing a block would require altering the entire chain.

Significance:

1. Decentralised Mechanism: Eliminating need for a 3rd Party to validate the transactions

2. Bringing Transparency and Efficiency: Any asset of Value can be represented and tracked

3. Fraud Prevention: Data stored in other places not easily accessible

4. Blockchain Business Value: WEF (World Economic Forum) anticipates 10% of Global GDP will be stored on blockchain by 2025

5. Applicability in Diverse Domains: Education Governance, Finance & Banking, Healthcare, Logistics, Cyber Security, Power Sector etc.

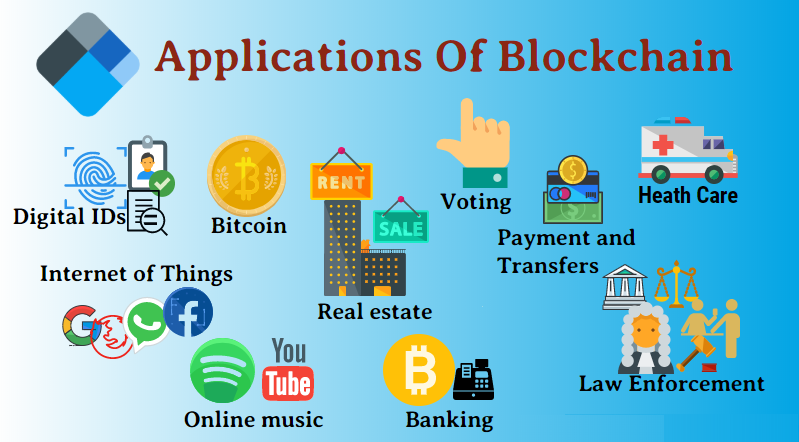

Applications:

1. Cryptocurrencies: Digital currencies like Bitcoin and Ethereum are built on blockchain technology, enabling secure and decentralized transactions

2. Smart Contract: Self-executing contracts with the terms directly written into code, automatically enforcing agreements

3. Supply Chain Management: Enhances transparency and traceability, reducing fraud and inefficiencies in supply chains

4. Healthcare: Securely stores patient records, ensuring privacy and interoperability

5. Voting System: Provides Secure and Transparent Method for Conducting Elections, Reducing Fraud

6. Identity Management: Self Sovereign Identity, Control over own personal data

7. E-Governance: Property Record Management, Digital Birth, Death and Education Certificates Management. Eg. Smart Dubai initiative of UAE

8. Law & Order: Blockchain based FIR Filing, Judicial Work, E-Courts etc.

9. Other Arenas: Automotive, Tourism, Insurance, Real Estate etc.

Benefits:

1. Enhanced Security: Cryptographic techniques provide strong security.

2. Transparency: Open and verifiable by anyone.

3. Reduced Costs: Eliminates intermediaries, reducing transaction costs.

4. Efficiency: Automated processes and faster transaction settlements

Challenges

1. Technological Challenges

a. Scalability: Current blockchains face issues with processing high volumes of transactions

b. Storage: Data becomes Perpetual and Replicated at all nodes

c. Latency: Time required to verify and add transactions to blockchain can be significant – late confirmation of transactions

2. Legal & Implementational Challenges

a. Privacy & Regulation: Legal and regulatory frameworks are still evolving

b. Localisation Hurdles: Replication across all nodes causes difficult to Localise to a certain area

3. Lack of Skill Set and Customer Awareness

4. High Energy Consumption: Environmental Concerns

5. Security Concerns:

a. Smart Contract Vulnerabilities: Bugs and vulnerabilities in smart contracts can lead to significant financial losses

b. 51% Attacks: Gaining control of more than 50% of Network’s Computational Power will lead to manipulation of blockchain = Lead to double spending and other security issues

6. Interoperability: Different blockchain platforms often operate in Silos, making it difficult to transfer assets or data between them

a. Need to develop standards and protocols for seamless integration

7. User Experience

a. Complexity: Need for good understanding of technology, barrier for non-technical users

b. Key Management: Users need to manage their private keys securely – losing can lead to loss of assets permanently

8. Cost:

a. Development and Maintenance: Costly and Scarce Skilled Workforce

b. Transaction Fee: High Network Congestion and drive prices up

9. Integration with Existing System can be Complex

10. Governance: Decentralised Decision Making can lead to difficulty in reaching consensus among diverse group

Potential Solutions/Way Forward:

1. 2 Layer Solution: Can help expand Throughput (No of Transactions)

2. Energy Efficient Consensus Mechanism

3. Regulatory Clarity

4. Interoperability Protocols

5. User Friendly Interfaces

6. Education Initiatives

Conclusion:

Conclusion 1:

Blockchain technology holds significant potential to transform various sectors in India by enhancing transparency, security, and efficiency. With the right regulatory framework and infrastructure in place, blockchain can drive innovation and contribute to the overall economic growth of the country.

Conclusion 2:

India's government is actively exploring blockchain's potential. The "National Strategy on Blockchain" by MeitY highlights its vision to adopt blockchain in various sectors to improve transparency, efficiency, and financial inclusion.

While blockchain offers a lot, it's still an evolving technology. Challenges like scalability and regulation need to be addressed for widespread adoption. But overall, blockchain holds immense promise for India's economic growth and social development.

Global Efforts Towards Blockchain Technology

1. China: Blockchain based identification system for its Smart City Infrastructure

2. EU: Cyber Security and Regulations

3. Estonia: Keyless Signature Infrastructure Blockchain Technology to authenticate Electronic Records

4. USA: Food and Drug Inspection – Solve Problem of Transparent and Security in Health Data Processing

5. UK: Uses Blockchain to track meat distribution to enhance food traceability

6. Brazil: Voting and Bidding for Projects

7. Singapore: Cross Border Payments and Securing Healthcare and related social data

8. Chile: Enable transparency in Energy Grid (tracking data and finances)

9. Zug, Switzerland: Accepts Bitcoin as Payments for taxation purposes. Also developed Blockchain based voting system and created Blockchain Task Force

10. Sweden: Real Estate Deals and Ghana Land Registry and Cadastral Register – collect property taxes

National Strategy on Blockchain

• Aims to Provide Trusted Digital Platform for providing e-Governance Services using blockchain technology

• Promoting Research and Development, Innovation, technology and application development

• Facilitating state of the art, transparent, secure and trusted digital service delivery system to citizens and businesses

• Virtual Currency such as Bitcoin, however has been kept out of the ambit of this framework

Conclusion:

Blockchain technology is still in its early stages, with significant potential for future development. It can address major issues in the Indian economy, such as underdevelopment, intermediary intervention, privacy concerns, financial transaction efficiency, and cybersecurity. The National Strategy on Blockchain Technology aims to leverage this technology for the country's holistic development. Proper implementation across all sectors is essential to achieve optimal outcomes.

Author: Arjun Kr. Paul, Faculty

Comments (0)

Categories

Recent posts

Q5/ Section B, APSC Mains 2024 Essay - ...

29 Jul 2024

Satellite Town

21 Jul 2024

Q 1/Section A, APSC Mains 2024 Essay - ...

29 Jul 2024